When Amazon launched a low-profile product called ElasTIc CompuTIng Cloud 12 years ago, the Internet industry across the ocean also ushered in an unprecedented development opportunity.

This year, the Chinese government portal officially opened at the beginning of the new year. In March, the State Council Informationization Leading Group issued the “Overall Framework for National E-Governmentâ€, which provided a top-level design for e-government development.

In this year, the number of Chinese netizens increased by 26 million to 137 million, breaking through 10% of the total population.

Also in this year, the number of Chinese websites increased by 150,000 a year, the total number exceeded 840,000; the total number of Chinese domain names has increased by nearly 20 million per month, with a rapid growth of domain names, 4.1 million domain names, and more CN domain names. Up to 1.8 million.

All these seemingly boring numbers have also made the best footnote for the development of the Chinese Internet and cloud computing. In the past 12 years, Amazon EC2 has grown from a small to a large, becoming the new growth engine of the Amazon Empire. The Chinese cloud computing industry has also ushered in a new life after years of struggle.

According to the Ministry of Industry and Information Technology's “Three-Year Action Plan for Cloud Computing Development (2017-2019)†last year, the total cloud computing industry will reach 430 billion yuan by 2019.

Such rare historical opportunities and huge market scale have also attracted more and more Internet giants, IT vendors and startups. In the past 2017, the Internet giants represented by Ali and Tencent have been public in the past year. The cloud market is staking, using the scale advantage of the public cloud to provoke a round of price wars; the startup companies represented by Jinshan and Qingyun are attacking the city in vertical areas such as games; Huawei has long cultivated private clouds for many years. In 2017, we also adopted a corporate restructuring to fully launch public cloud services.

The general consensus in the industry is that there is no single big situation in the public cloud market or the private cloud field. This is determined by the market capacity. Just like the US market, although Amazon AWS has already been riding the dust, Giants such as Microsoft and Google still occupy a large market share.

On the other hand, focusing on the evolutionary path of cloud computing still needs to start from several giants. After all, as the proportion of enterprise cloud service spending in the entire IT expenditure is getting higher, the demand for cloud services is becoming urgent. In view of the hardware, computer room, operation and maintenance and pre-sales and sales of cloud service head manufacturers, these giants are building a brand new moat.

Next, I will take Alibaba, Huawei and Tencent as examples, from the beginning of the layout, to the mid-range trend and possible endings, to sort out the status quo and future of cloud computing with Chinese characteristics.

layout

In the rules of Go, the importance of the layout is self-evident. At this stage, the players each seize the open space on the board and try to prevent the other party from occupying the land.

The same is true in the field of cloud computing. Amazon's first-mover advantage in the world comes from its early deployment. In China's cloud computing market, Ali, Huawei and Tencent almost all entered the cloud computing market around 2010.

According to public information, Alibaba Cloud was established in September 2009, and its early stage was mainly for Ali's internal business services. Until May 2010, Alibaba Cloud's cloud server officially began to serve externally. Also in 2010, Huawei and Tencent also released cloud strategies.

In the slightly "distant" 2010, when Li Yanhong did not believe that cloud computing and Ma Huateng cloud computing were too early, in fact, only Ali and Huawei regarded cloud computing as the next key development strategy. In the face of Li Yanhong and Ma Huateng, Ma Yun said: "Our own company is full of confidence and hope for cloud computing... Alibaba has a large amount of consumer data and Alipay transaction data. We feel that this data is useful to us and more useful to society."

Huawei used a press conference to announce the official launch of cloud computing. In November 2010, Huawei officially released its global cloud computing strategy and end-to-end solution. It hopes that through the launch of the open cloud computing platform, customers will use ICT applications such as data center, computing and storage resource sharing like electricity.

If Ma Yun’s plan for the development of Alibaba Cloud Computing was to digest and upgrade the internal massive data, then Huawei, who has been deeply involved in the telecom service field for many years, may have already seen the significance of the cloud in Huawei and the IT industry. Ren Zhengfei In a speech in November 2010, he asserted: "The future of information networks is actually simplified to two things, one is the pipeline and the other is the cloud."

Just as the influence of the player's layout on the mid-range, the many things that happened in 2010 also partly determine the strategic layout of each company in the next few years. Ali's advantage in data promotes the layout of Alibaba Cloud computing business at the data level. It has released Maxcompute for data processing and the digital plus platform for big data applications. Huawei has integrated its internal environment through its own ecological and soft and hard integration advantages. Server, storage resources, launched a series of integrated solutions; and the development of Tencent Cloud, although long-term free in the media spotlight, but relying on its technology accumulation in the game, payment field and mass users, gradually obtained in these areas breakthrough.

Mid-War Battle 1: Data Center Distribution

Chess to the middle plate, the advantages and disadvantages of each family gradually emerged. Looking at the data center distribution first, for cloud computing vendors, the diversified data center layout is self-evident. On the one hand, it is necessary to ensure the normal operation and maintenance of cloud services, and at the same time, it can also flexibly control data protection. In addition, it is the user experience. In some applications of enterprises, there are high requirements for user response time. By storing data close to the enterprise's data center, you can minimize user delays.

As a result, the number of data centers once became a focus of the giants to promote their own cloud computing.

The picture below shows the current data center distribution of Alibaba Cloud. It can be seen that in addition to the Chinese market, Alibaba Cloud also values ​​South Asia and Southeast Asia.

In the global infrastructure map approved by Tencent Cloud, there are still many overseas cooperation infrastructures. This is actually quite a clever argument. In other words, this is the service facility leased by Tencent.

In March 2018, with the official opening of the Hong Kong node, Huawei Cloud's Asia-Pacific market also started. Compared with Ali, Tencent and other companies that have public cloud, Huawei's data center layout is more reflected in its partner cloud with many partners, such as through cooperation with Deutsche Telekom and Orange France Telecom. The open cloud platform across Europe, and the cooperation with Telefonica, will expand Huawei's cloud business to Latin America.

As globalization deepens, more and more enterprises need global data and computing platforms. In order to meet these needs, cloud service providers will continue to compete for more data centers and service areas.

In the middle of the war 2: private cloud becomes a product variable

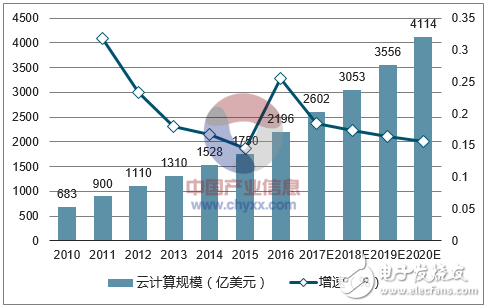

The media’s promotion of cloud computing “products†has long been equated with public cloud products. Part of the reason for this misleading propaganda is that the US cloud computing standard is placed in the Chinese market. The following picture is from the China Industrial Information Network. It can be seen that the global market size of the public cloud is indeed very gratifying.

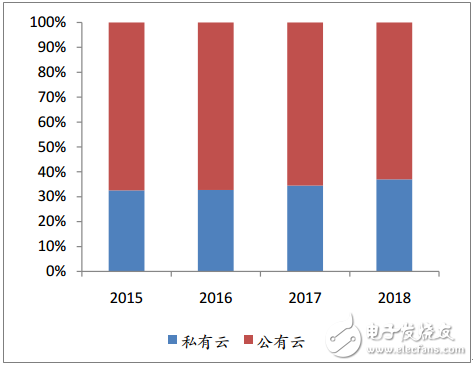

In the US market, the public cloud has obvious advantages, which is a data of Zhiyan Consulting.

But "public cloud is cloud computing" is obviously only a regional statement. In China, the pattern between public and private clouds is obviously another version of the story.

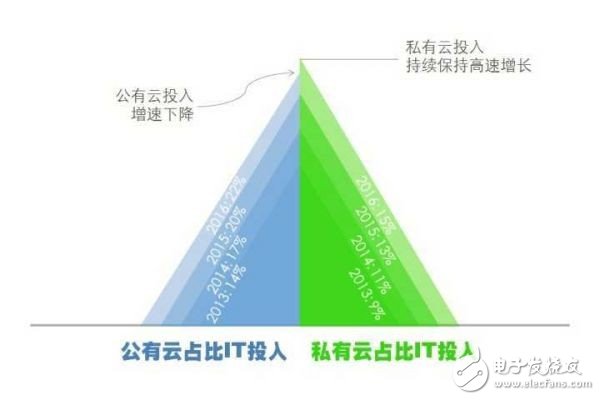

In fact, if you look closely at the size of the public cloud and private cloud in the US, you may also find that although the public cloud accounts for nearly 60% of the total, the market size of the private cloud is gradually expanding.

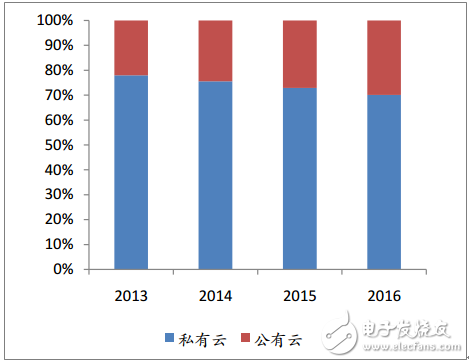

Similar conclusions can also be made in the "Internet Queen" Mary. In Mikel's 2017 Internet Trend Report, as shown in the following figure, the private cloud's year-on-year growth rate was higher than that of the public cloud in the three years from 2014 to 2016. In 2016, the private cloud increased over the same period as the public cloud. It is 5.39 percentage points higher.

The reasons for such a big difference between China and the United States are also very complicated. For example, many Chinese companies, especially large enterprises, have long had their own IT construction routes and specifications, and have high requirements for business needs and data security. Public cloud service providers in the market cannot meet their needs, so private clouds are needed. Achieve efficient operations of the business.

According to a data from the China Institute of Information and Communication, in 2016, China's private cloud market reached 34.48 billion yuan, an increase of 25.1% compared with 2015. It is expected that China's private cloud market will continue to grow steadily from 2017 to 2020, by 2020. The market size will reach 76.24 billion yuan.

The above trends can also be seen from the strategic adjustments of the major players. Alibaba Cloud, which started from public cloud, released the Apsara Stack in April 2016, enabling enterprise customers to deploy Alibaba Cloud's cloud operating system in their own data centers.

Tencent launched its private cloud solution in early 2018: TCE (Tencent Cloud Enterprise). This product provides a complete solution for network and database to service for large and medium enterprises.

Huawei has more say in the private cloud space. In 2013, Huawei released FusionSphere and FusionInsight for virtualization and big data. According to IDC, FusionSphere virtualization solutions ranked first in China's OpenStack software market and China's server virtualization market. In Gartner's DMSA Magic Quadrant Research Report, FusionInsight entered the DMSA Magic Quadrant's specific quadrant.

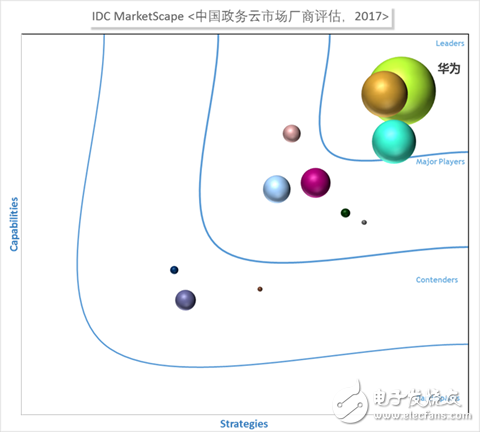

All this has also given Huawei's private cloud product FusionCloud a greater confidence. In the field of government affairs cloud, in the IDC report, Huawei Cloud Government Cloud Solution is ranked among the leaders of China's government cloud market, regardless of its existing capabilities, future strategy and market performance.

However, just as the public cloud is not the whole story, the private cloud is only an integral part of cloud computing. In a sense, Alibaba Cloud enters the private cloud market and establishes Cloud BU with Huawei. The purpose is the same, that is, to seize the whole The field of cloud computing.

Today, the public cloud market for cloud computing has a new variable, artificial intelligence.

In the middle of the war 3: When the public cloud hits artificial intelligence

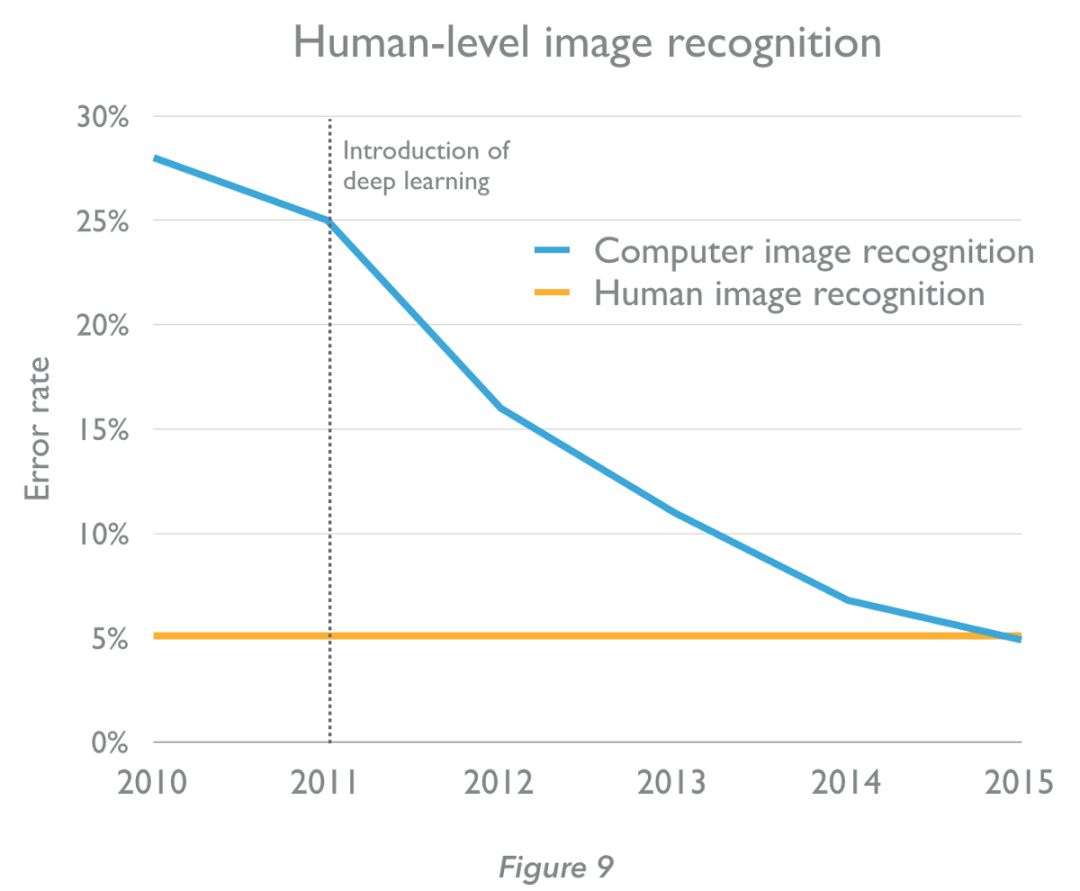

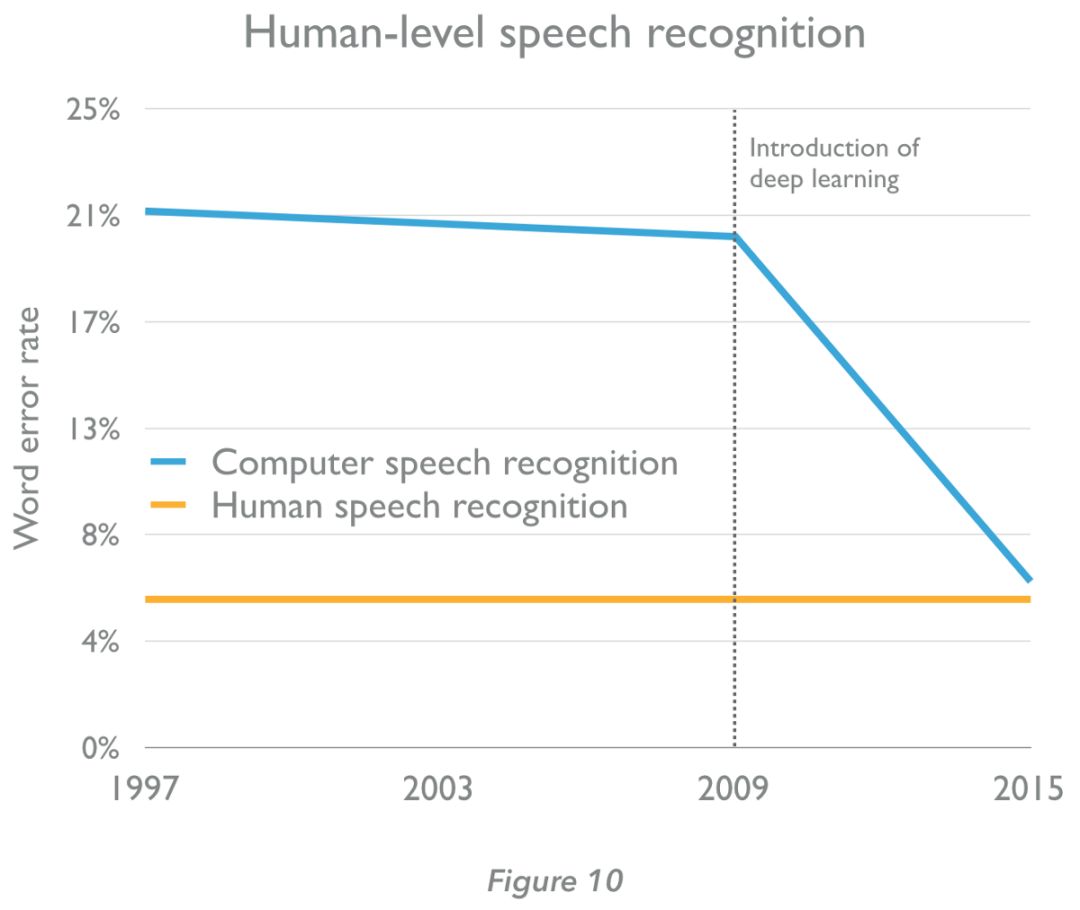

Artificial intelligence is not a new concept, not even an accurate concept, but the artificial intelligence technologies represented by deep learning bring new surprises to the entire technology industry. Among them, the development of image and speech recognition is particularly prominent. The following figure is a data of the European investment company MMC, showing that the machine has partially surpassed humans in the field of image and speech.

However, both image recognition and speech recognition require huge up-front investment, including hardware (such as GPU purchases) and personnel (high-level artificial intelligence talent is very expensive). This is precisely the best product for cloud services. Through the scale advantage of the public cloud, the development and application cost of artificial intelligence can be greatly reduced, thus promoting the popularization of related technologies.

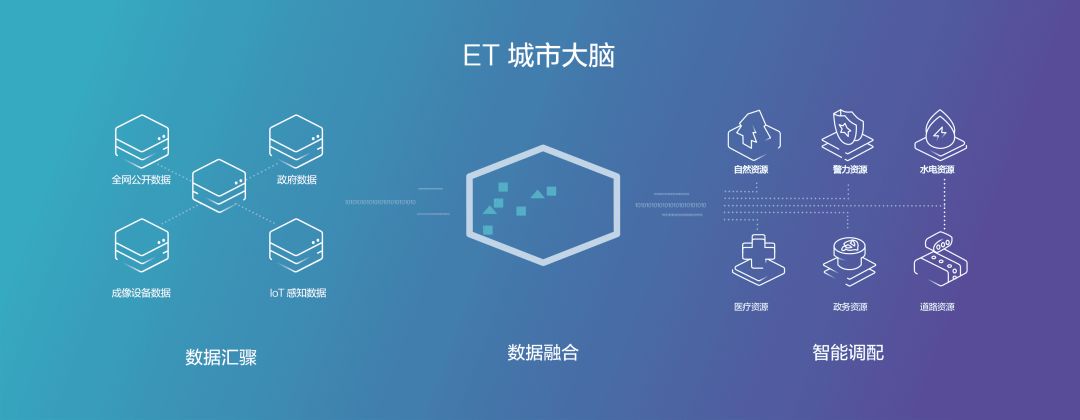

Beginning in 2016, Alibaba Cloud began to increase the artificial intelligence elements on public clouds. At the Yunqi Conference in October of that year, Alibaba Cloud launched the ET City Brain. The key is to form a more optimized solution based on the analysis of urban traffic data, especially traffic camera surveillance video/image data.

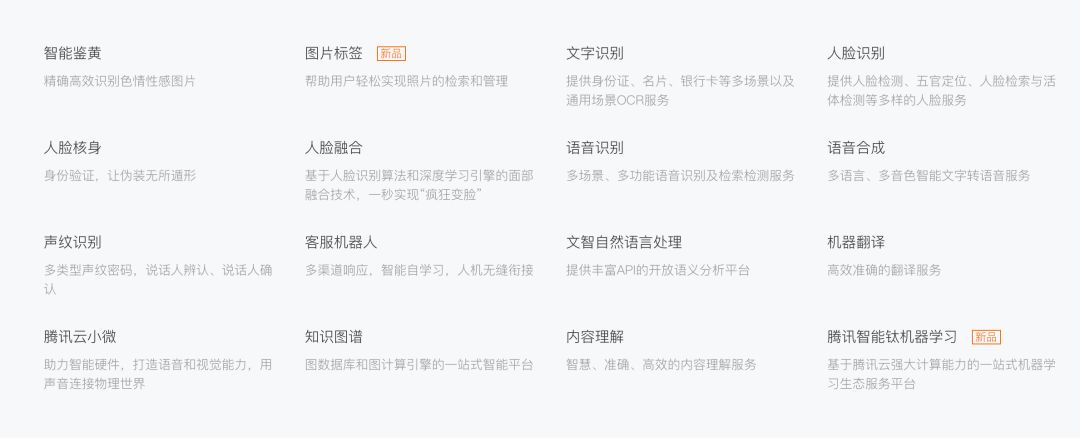

Subsequently, Alibaba Cloud continued to extend the ET brain to industries, environments and other fields. Similarly, at the Tencent Cloud Summit in 2017, Ma Huateng personally staged and released the strategic product "Smart Cloud", announcing the opening of Tencent's three core competencies in computer vision, intelligent speech recognition and natural language processing. The picture below is Tencent Cloud. Artificial intelligence products provided.

In Ma Huateng's view, artificial intelligence and cloud computing are almost "perfect". In other words, the best way to land cloud computing is artificial intelligence. "Cloud is the strong carrier of artificial intelligence" has become a direction for the development of Tencent Cloud. one.

Huawei Cloud has also made great achievements in the field of artificial intelligence. Due to Huawei's own corporate attributes, its extensive experience in the manufacturing industry has contributed to the emergence of Huawei Cloud EI (Enterprise Intelligence). The following figure shows the basic architecture of Huawei Cloud EI. From the computing layer, data layer, platform layer and application layer, a set of artificial intelligence open platform based on public cloud is built.

In fact, the artificial cloud products of public clouds are being homogenized. This is of course due to the limitations of individual technologies of artificial intelligence. The more important challenge is how to combine these single-point technologies with industry scenarios. How to win the benchmark of the industry is the key.

In the case of Ali, the urban solution based on ET brain has been landed in Hangzhou and other places, and will be extended to Macau and Kuala Lumpur at the end of 2017 and early 2018. In the industrial field, GCL Solar and Zhongce Rubber have also been adopted.

Compared with Alibaba Cloud's echelon-style operations in urban and industrial fields, Tencent Cloud's artificial intelligence has come to fruition. For example, in cooperation with SF Express, OCR is applied to the identification of express delivery orders. For example, Tencent combines cloud face recognition technology with the security cameras of various public security departments.

Huawei Cloud's artificial intelligence product EI also plays the role of intelligent engine among many large enterprises. According to public information, Huawei Cloud EI's customer base includes finance, telecommunications, and safe city. It is worth noting that Huawei's long-term strategy of “cloud-end-management†has also brought synergy to the implementation of cloud-based artificial intelligence products. For example, in cooperation with PSA Peugeot Citroen, Huawei combined its own global cloud revenue practices with deep learning algorithms to form a car network support platform with “end pipe cloud + business support systemâ€. The Citroen DS7 Crossback model of the Internet of Vehicles technology.

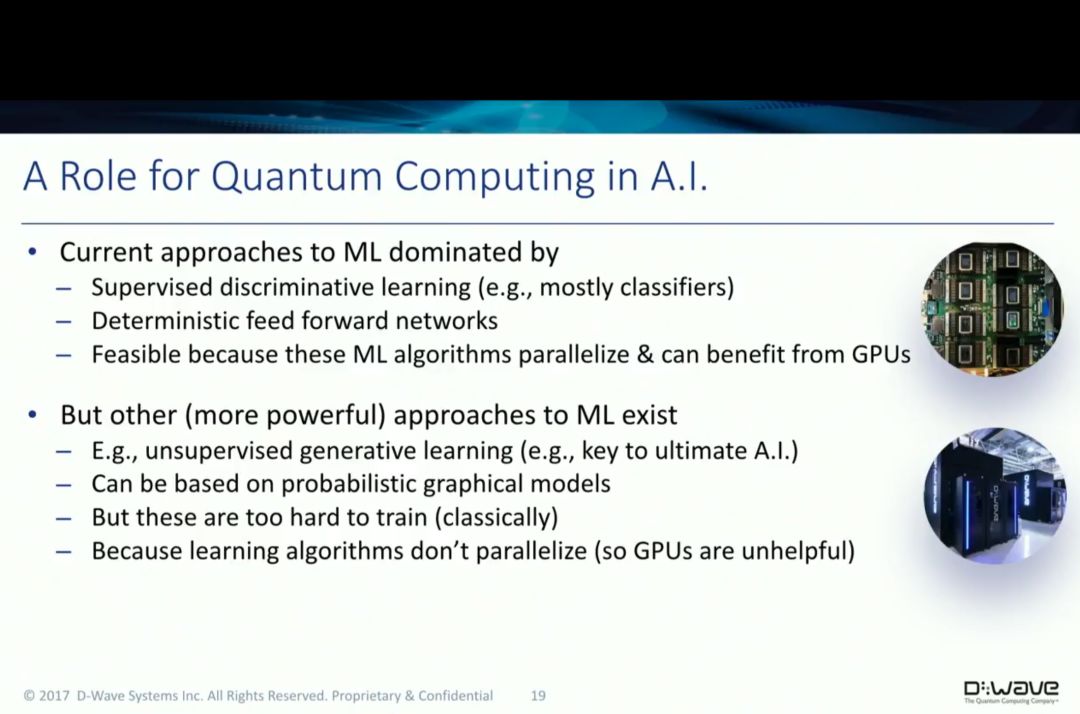

After several years of speculation, the industry's judgment on artificial intelligence has basically tended to be the same, that is, this round of artificial intelligence is still in the early stage: in addition to deep learning, new algorithms such as reinforcement learning and confrontation generation networks are also Progress has been made in different fields; GPUs, CPUs, FPGAs, and other proprietary chips have not yet been finalized; the gratifying progress of quantum computer research has given more imagination to the future of artificial intelligence. The following figure is the quantum computer startup D- Wave's view.

This also means that the artificial cloud war of the public cloud has just begun. In the United States, Google uses artificial intelligence on the cloud, especially machine learning products, to quickly catch up with Microsoft and Amazon, and Amazon is also "renovating" itself. Cloud services; in China, the AI ​​pattern on the cloud is also in the middle stage of the cloud industry as a whole, and there will be many factors worthy of attention in the future.

What happens from the middle to the end?

Like the development of any technology in the past, when cloud computing comes to an end, it is also the time when cloud computing truly becomes the infrastructure for social and economic development. At that time, the so-called cloud no longer has a public cloud, a private cloud, a unified platform unified architecture, the flow of encrypted data, enterprises, developers through the cloud service API to obtain secondary development resources, ordinary Users can enjoy smart, secure cloud services for a small fee.

However, judging from the strategic layout of the previous period and the short-selling of the mid-range products, there is still a long way to go from the final stage of cloud computing in China, and there are still many uncertainties.

First, data compliance and security. In China, the reason why the private cloud market is so strong is that enterprises have great concerns about the core data, especially in large enterprises. To this end, Ali, Tencent and other Internet companies continue to prove their security capabilities through external data security certification. Huawei further emphasizes the boundaries of cloud service providers in addition to external security certification: not touching applications, not touching data, not doing Equity investment in cloud services.

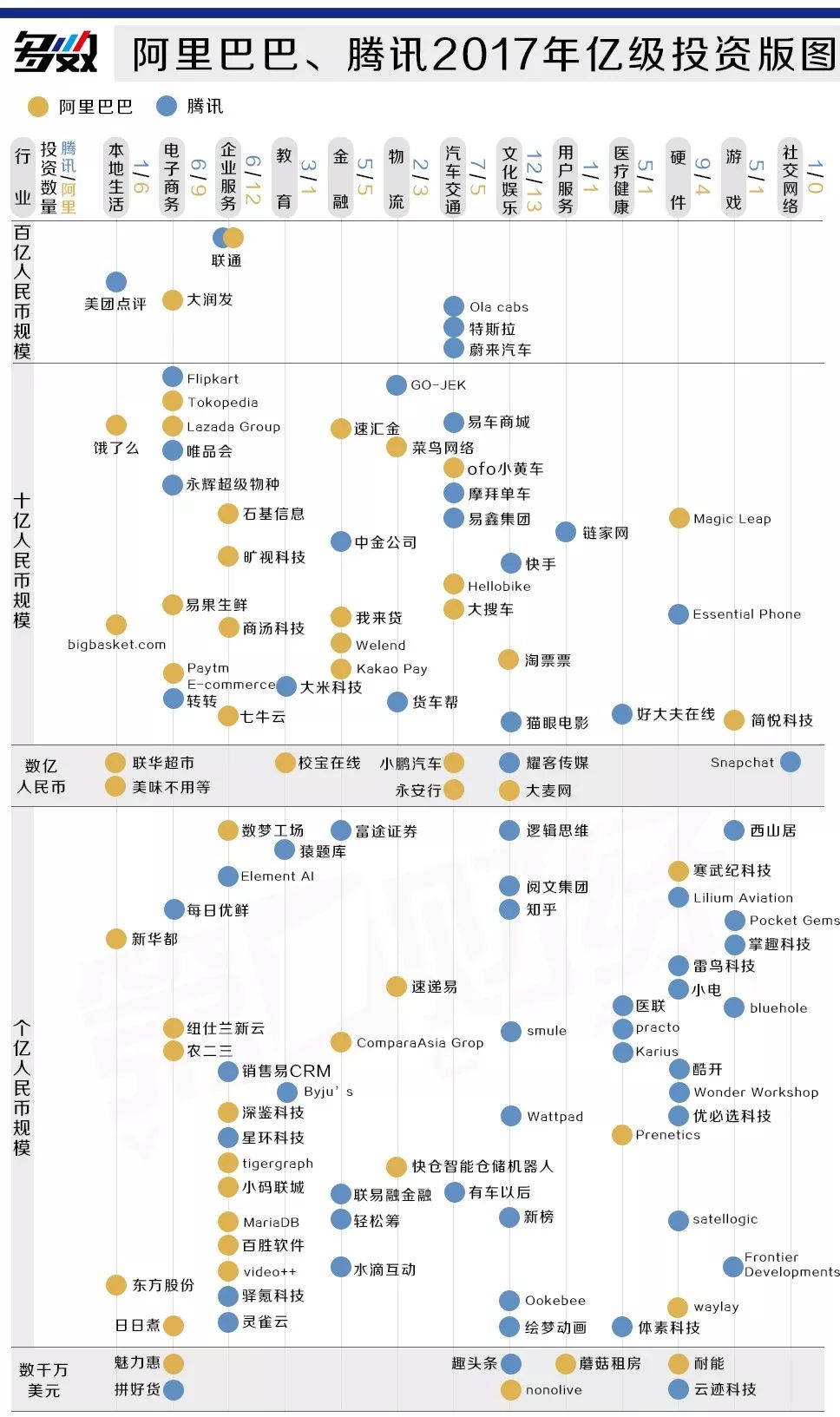

This also leads to the second uncertainty factor, whether the cloud ecology that the giants say is open or win-win or closed garden. Considering the special situation of China's Internet, in the past few years, Ali and Tencent have used investment, acquisition, joint venture, etc., and their products or services almost involve ordinary Chinese people's daily food, clothing, housing and transportation. The following picture only reflects the two companies in 2017. Investment map.

The layout of these investments or joint ventures has also raised the question of the neutrality of the cloud services of the two companies. It is almost impossible for a company invested by Ali to use Tencent Cloud, and a company invested by Tencent will not choose Alibaba Cloud. This artificially fragmented cloud service has also shaped a new Chinese cloud service format.

From this point of view, the importance of neutral manufacturers represented by Huawei Cloud is becoming more and more obvious. These neutral vendors stand in the perspective of industry or enterprise enablers, and build a complete set of public and private cloud systems through open architectures such as Openstack, which can maximize the productivity of enterprises after the cloud.

Third, cloud computing is essentially a service industry, but it is covered with high-tech outerwear. Traditional IT products can be "products (software, hardware) + services", while cloud products are services from pre-sales, sales, and after-sales. The so-called "X-as-a-service" is the case.

This is a huge challenge for Internet companies that have historically relied on traffic. There was a question on Quora that mentioned why Facebook did not set up a cloud computing business. The answer is simple, because Facebook can't form an offline engineer service team.

Facebook's challenge is also a problem faced by Chinese Internet companies such as Ali and Tencent. In fact, during the development of Alibaba Cloud, Alibaba's acquisition of Wanwang in 2009 was indispensable. Wanwang not only brought a large number of SME users to Alibaba Cloud, but also brought a wealth of offline service experience to this Internet-based company.

Huawei, which has been working on IT products for many years, has an advantage in the online service market. According to public information, Huawei has an offline support team in 170 countries and regions. How a global service network of scale and volume will be integrated into public cloud services will become a key factor for Huawei's rapid development.

Finally, there is a technical reserve. Cloud computing is a comprehensive technology platform that covers everything from hardware and software to algorithms and customer service. When Google's DeepMind used artificial intelligence algorithms to optimize room power consumption, Ali also showed servers that were fully immersed in water, and Huawei relied on its own strong research and development in the server field, fully recognizing that existing X86-centric architectures could not In response to new business such as AI, we need to move towards an era where heterogeneous architecture is at the core. Therefore, through Atlas through key technologies such as heterogeneous resource pools and intelligent orchestration, resources such as X86, GPU, FPGA, and storage can be pooled, and unified scheduling and scheduling can be performed after remote access, thereby providing hardware resources on demand, increasing by more than 50%. Resource utilization, significantly reducing hardware models.

The reserves and research and development of these black technologies and new technologies will greatly improve the operational efficiency of cloud service providers, while further reducing costs. The ultimate goal is to minimize the threshold of cloud computing and make the various services of cloud computing Huihua.

Written at the end

If you start EC2 from Amazon, cloud computing is only 12 years old. Today, the Amazon Web Services (AWS), which was used to solve Amazon's idle resources, has become an industry with nearly $20 billion in revenue a year.

More importantly, this is still a fast-growing market. In the US market, Amazon, Google and Microsoft have released earnings reports, and revenue from cloud services is growing substantially. In the Chinese market, the special IT industry environment and policy regulations are a huge benefit for the majority of Chinese cloud computing companies. In the above, through the typical representatives, the layout and product layout of Alibaba Cloud, Tencent Cloud and Huawei Cloud The disk has already presented the realistic picture of China's current cloud computing.

For the future, data security and compliance are not difficult. However, the contradiction between the ecological advantages of the Internet giants such as Ali and Tencent and the inability to neutralize cloud services is almost irreconcilable. This also makes the neutral manufacturers represented by Huawei more competitive. force. The speed and direction of the evolution of artificial intelligence technologies will continue to increase the uncertainty of the cloud service competition. The game of this cloud service will also present more exciting games.

Paperlike Screen Protector For IPad

Paperlike Screen Protector,iPad Paperlike Screen Protector,Paperlike Screen Protector iPad

Shenzhen Jianjiantong Technology Co., Ltd. , https://www.tpuscreenprotector.com